Previously the responses had been almost completely draconian and totalitarian – the removal of children from religious homes, the criminalization of public religiosity such as prayer or evangelism, the banning of religious owned property and the requirement of state sanctioned (and thus purely secular and atheistic) education and curriculum in all education settings from public schools to charter schools and even home schools. The only thing missing from this was the hammer and sickle and someone leading the effort that goes by the title Chairman. Truly a testament about what happens when we forget the past and exactly how totalitarian regimes take root.

Thankfully 5 years later, much of that was gone. Of course some of those answers came in – religious upbringing is child abuse, specifically the doctrine of hell; religion is mental illness and the state should mandate treatment; only secular state run education; and all of that. Anti-theists and atheistic fundamentalists are probably going to be a mainstay among us for as long as religious fundamentalism will be. However, these answers did not dominate the conversation like they had in the previous survey. The primary response was the removal of the tax exempt status of churches and religious organizations. It is to this topic that I will turn.

The history of tax exemptions and the organization of a non-profit sector is long and complicated and I am far from an expert in this area. This is a very helpful resource for those who would like to delve into the broader history of tax law. Rather than focus on how we get here, I’m going to simply clear up some misunderstandings and why ending tax exemption for churches is not only problematic, but may actually end up working against the separation of church and state in the long run.

I would like to begin by clearing up one major myth the seemed to crop up throughout the answers as to why revoking tax exemptions would be preferable – I’m going to call it the Joel Osteen Myth. This is the idea that Churches are money making machines to bilk their congregation of their hard earned money. Joel Osteen and his $10M+ home was used regularly as exhibit A for this myth. Anyone who knows me knows that I am not an Osteen fan, not in the slightest. I’m a harsh critic actually – mostly for theological reasons however (which I actually think are more substantive than political or cultural ones). However, I also think that if we are going to be critical and use this man as an object lesson for ecclesiastical greed, we should also be accurate. My comments should not be read as endorsing that pastors should be that wealthy or that it’s ethical for a church to be so well off or even that big. That’s not the point I’m making, but rather that Osteen and megachurches everywhere are not a good reason to cut tax exemption – it would be an exemplar of cutting off the nose to spite the face.

We need to remember that Joel Osteen is a brand more than a pastor. He has a publishing and product empire that is surely the main source of his income. I was reminded of Rick Warren who became wealthy after his book The Purpose Driven Life topped the best seller charts, and then not only stopped drawing a salary from Saddleback Church where he pastored, but also cut them a check to pay them back for all of the pay he had drawn from them over the year. I wondered if Osteen had done something similar and sure enough, he stopped drawing a salary from Lakewood shortly after his first best seller. So when we look at Osteen’s house or wealth, we should realize that his publication, not his pastorate, is almost certainly the source. At his peak, he was drawing about $200k annually as a salary. Now is that a lot? Well without getting into too much evaluation of the ethics of pay, that would put him at average for upper middle class. He would not even have been classified as Upper Class yet if his salary from Lakewood was his only income. Clergy taxation is also very complicated with housing allowances, personal tax, self-employment clergy tax, and so forth. So we should also keep in our minds that the tax exemption of churches is not the same issue as the tax burden of clergy.

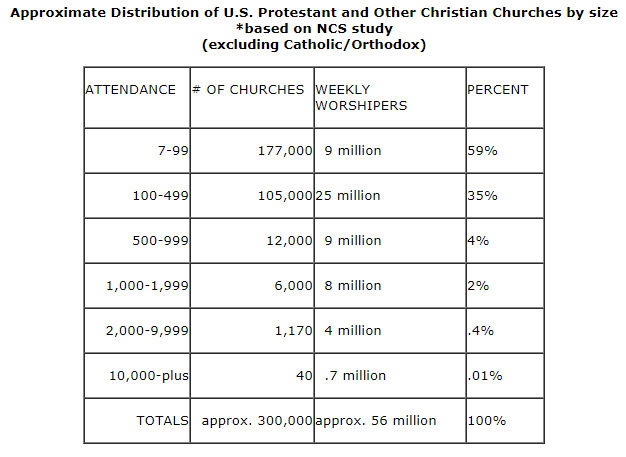

Next, does Osteen’s wealth warrant the argument that his church (or all churches) should be tax liable? If this were the case, then a large number of nonprofits would fall under the same argument. We will get to this shortly when we discuss the nature of a nonprofit but it would be a problematic argument to say that if the leadership of a nonprofit is well paid, then the organization itself should no longer be a tax exempt nonprofit. We will discuss this in more detail shortly. What the Joel Osteen Fallacy relies on is the assumption that wealthy churches and pastors are the norm, or are at least representative enough to rightly depict church financial practices as a whole. This is a myth large enough to plant a megachurch in. As we can see from the stats in the graphic below drawn from a study done by The Hartford Institute:

A megachurch is typically classed as 500 members and above. This means that approx. 6.5% of all churches in the U.S. are megachurches. The average church in the U.S. is under 100 people. And what about salary? The average pastor’s entire compensation package (salary and housing benefit) is $31k – if he has two children, that would be barely above the poverty line. Roman Catholic priests earn somewhere between $21k to $26k – no kids to worry about so further from the single person poverty line but not by much. Jewish Rabbis are the highest paid earning more than the average protestant pastor and Catholic priest combined. This means that the average clergy earn over $20k less than the average public school teacher at $59k. Now the atheist may think that it is good that educators earn more than pastors (what with all deluding of the minds of our congregants), but they should not then think that churches are money making machines or that most clergy do it for the financial advantages of it all. In fact, the average salary of megachurch pastors serving in churches of 1000+ (the top 2.5% of church size and only about the top 1/3 of all megachurches) had an average total compensation package of only $81,923. So even when we explore the largest and wealthiest of U.S. churches, we are not looking at people living fat on the calf so to speak. And once we break down salary from housing benefit, their actual take home pay may be well below those numbers.

With that leg of support for the demand for tax exemption to be revoke effectively swept away, I would like to address another major area of confusion. Churches are a non-profit organization which confers certain tax benefits. However they are a specific type of non-profit – a charity. Let’s break these down first explore some of the problems that may arise from trying to remove tax exemptions for churches only.

A nonprofit is any organization where its net profit from donations, fees, or any other revenue from activities does not go to the benefit of any one or multiple individuals. This means, basically, that the profit goes back into the operation of the organization rather than going into anyone’s bank account or paying off shareholders. Nonprofits do not need to serve the general public and can charge for services – a very well-known example that we will use as a paradigm for this discussion, is Planned Parenthood. They have a very well paid leadership, take government subsidies, charge for services, make voluminous profits, and yet because all of the profit goes back into the operation of the organization and not to the payment of any individual(s).

Planned Parenthood is not only a nonprofit though – they are a 501(c)(3) nonprofit: a charity. This is the same category as a church in fact. A charity is a nonprofit whose purpose is to benefit the public at large and aim to improve the quality of life of the community somehow. On helpful way to think of the difference between a general 501(c) nonprofit and a charity 501(c)(3) is the scope of work that they do. Where a nonprofit generally can market itself to a certain group of paid members (homeowners associations and auto clubs are a good example), specific charitable nonprofits exist to serve the general public in some way. In essence, general nonprofits can be specific while specific nonprofits must be general. Clear as mud?

Several other myths that I hear from atheists frequently can now easily be dispatched when we use Planned Parenthood as the paradigm. A common myth is that a charity is classified by how much of its earned income that it gives away (I commonly see an arbitrary 80% number thrown around) but this is simply not the case. Do atheists think that Planned Parenthood gives away 80% of its earned revenue (not just profit) to the community? Clearly they do not.

Another myth is the Joel Osteen Fallacy discussed above, and that is that if the leadership is well paid (or I heard if they even had paid full time leadership at all) that they should lose their tax exemption. The current CEO of Planned Parenthood, makes over $500k per year – 2.5 times what Osteen earned and over 6 times what the average megachurch pastors earned. There are other charity CEOs that are in the millions. If a charity needs to have its tax exemption revoked because of salary, then countless charities would need to be cut by that scalpel.

So, what about revoking tax exemption for churches? This brings up a lot of great questions and to be honest, if done equitably and consistently, I can see the arguments for both sides, even though I ultimately come down that tax exemption is the best for all parties. We will look at this through several landmines that arise from churches having their 501(c)(3) status revoked and becoming tax liable (specifically property tax) as well as some of the problems of them being classified as 501(c)(3). Basically, both are attempts to procure the separation of church and state but neither does it perfectly. (For a lengthier list of Pros and Cons of this issue, see here).

We will look at this from 3 angles: 1) Protection of the separation church and state, 2) protection of the right to exist as a church body, and 3) equitable regulations without unconstitutional religious tests.

1. Protection of the separation church and state. What many people do not realize is that as a 501(c)(3), individual churches are not technically permitted to endorse any specific candidate or to lobby congress. While there are broader guidelines on what kind of public support that they can show for policies or propositions, the tax law is clear – they cannot financially and officially endorse any candidate for public office.

This is known but not commonly understand, and considering that other 501(c)(3)s such as Planned Parenthood and the NRA are known for their lobbying efforts, this seems inconsistent. Isnt the evangelical lobby a huge driver in American politics? Well yes, but in these cases, the organizations that fund campaigns and lobby congress are not churches – they are not even 501(c)(3)s. They are often 501(c)(4)s or some other kind of nonprofit or charity that is permitted to endorse candidates and lobby and simply work on behalf of their constituents (Planned Parenthood and the NRA effectively set up shell charities that are not 501(c)(3) to do what they want to do) because they do not have the same set of tax exemptions that the 501(c)(3)s have with regard to property taxes.

So while there are loop holes, what the tax exemption allows is a clearer wall of separation of powers between Magisterial and Ecclesiastical institutions. The government is not using taxes on the church to fund things that would directly violate church beliefs, but the church is also not allowed to try and wag the political dog through lobbying and pulpit pounding. Both sides win.

On the other hand however, we can see in cases like the IRS’ fight with the Church of Scientology how tax exemption could still muddy the waters and allow the state to govern who is and who is not an officially sanctioned religious body. While they do have a set of guidelines for determining what counts as a valid ecclesiastical body (regular services, educational courses for members and children, regular and publicly known meeting locations, and about a dozen other factors), the IRS took the stance for approximately 30 years that the Church of Scientology was not an official body despite meeting nearly all or most of the criteria on their list, mostly because the methods of the church ran too much like a business and it was demonstrated that funds were in fact being funneled directly to the profit of individuals. In 1993, the IS finally reversed this ruling and granted exemption status despite protest that their practices had not fundamentally changed.

While many of us would agree with the concerns over Scientology specifically, this incident does highlight an area where we may equally be uncomfortable giving the government authority – deciding what religions do and do not count as state sanctioned. It feels rather Red Nation to many of us – secularists included who worry that if the political pendulum would swing, that secular charities may be refused exemption. So for many, in the name of removing that authority from the government, the only way to resolve it would be to not even place it in the position to decide. This could be accomplished by not giving any charity that level of tax exemption such that the government wouldn’t be the one deciding – if we cannot play nicely, then no one gets to play, so to speak.

As of right now, the IRS takes a very hands off approach to classification. Basically, a religious body can assume to be tax exempt at their formation. They do not need to apply to be tax exempt. This allows for one of the more controversial issues in this whole debate – the lack of filing. Unregistered churches are assumed tax exempt unless proven otherwise, but since they are unregistered, they do not need to file their income with the IRS with the dreaded IRS form 990 or 990 EZ. That is clearly a major benefit to a religious or secular organization. However, there is a major downside – a risk. They are not officially sanctioned by the IRS. They have not been confirmed to be tax exempt. This means that they are in fact, in limbo. While many churches in major denominations can likely rest assured that they would qualify, smaller or independent churches or religious groups may not be so lucky. Imagine operating under the assumption that you are tax exempt, only to find out that you do not qualify. The back taxes could be astronomical. While it is highly unlikely, one could also conceive of a move by a more secularist anti-clerical government to arise and require registration with the intent of denying any unregistered religious groups. This would be quite a sizable financial and property/land grab since the back taxes would plausibly shut down a vast majority of religious organizations. So yes, they do not need to register and file, but they do so at some risk.

This leads naturally to the second issue – right to exist.

2. Protection of the right to exist. As many political commentators and economists have pointed out, the truism is true – taxation is the power to destroy. The problem here is rather simple – many churches simply would not be able to survive without the tax exemption. As we saw above, it is a myth that most churches are flush with money or even financially stable from year to year. Anyone who has been to small churches for some time know that often at the end of the year there is an extra push for giving – not to make the pastor rich, but to literally keep the lights on and the other bills paid. I’ve been to churches where the pastor, who already works another job, refuses to draw a salary for a month to make sure that the doors can stay open the following month. If churches who had been tax free for decades or centuries were suddenly forced to pay for taxes, many would simply not be able to remain open.

Another issue here is that of double taxation. Essentially a church (or really any 501(c)(3)) is a voluntary association where people pool resources for some community and/or public benefit(s). If the giving of the church is then taxed, effectively you are taxing that voluntary group of people twice. If the tax exemption 501(c)(3) status is revoked, then giving to that organization would be a taxable payment, not a charitable donation and as such you would be taxing the monies coming and going.

While this is almost the same as #1, allowing 501(c)(3)s to be taxed may run into the problem of the government deciding which religious organizations (or really which charities generally) could exist or not. Instead of deciding from the beginning who could and could not be considered a 501(c)(3), the government could create targeted taxation upon specific kinds of charities or land ownership if taxation was permitted.

3. Equitable regulations without unconstitutional religious tests. The issue here has been hinted at above. How would one go about determining which charitable and/or religious organizations and nonprofits would lose their tax exemptions? What would the standard and the metric be? If one argues that it should only be churches or religious organizations that should lose tax exemptions (this was the view of most of the atheists that answers the questions, typically explained as due to their belief that religion served no community good and harmed young people), then how would this process go about without an expressly stated religious test – which are deemed unconstitutional as an explicit violation of the 1st amendment? This kind of religious test would set an extremely problematic precedent – one even many secularists should be concerned with should the government swing more in favor of a more overtly religious or theocratic state.

There is a way around this though and that would be to remove tax exemptions equally across all 501(c)(3)s, shore up some of the ability to create shell organizations like 501(c)(4)s, or even back out many of the tax exemptions for nonprofits generally. However, in order to achieve this equitably the line in the sand would need to be around nonprofit classifications and not expressly religious lines. The atheists then who answered that revoking tax exemptions would need to think about if effectively overhauling and removing tax breaks for charities is worth what they think they would accomplish by removing tax exemptions from churches.

There are certainly more pros and cons that what I have had time to very briefly discuss here. Estimated revenues from property tax alone would be in the tens of billions annually – for some cities upwards of 80% of land is non-taxable so the boost in revenue would certainly be helpful. Ye t this too comes at a cost. Many churches operate soup kitchens, homeless shelters, free counseling services, community aid programs, etc. and if these services were to close down, the municipality may be tasked with paying for some kind of replacement services. In some cases, this may drive more cost to the government than it does revenue. It simply is not as clear cut as some would think, especially in more urban or rural environments where many of these small churches exist which would be disproportionately hindered.

Other issues arise as well when we enter into political and economic philosophy – is a tax exemption the same thing as a subsidy? Some say yes, some say no. I’m inclined to think that either view is possible to maintain but that if religious organizations (including atheistic and secular groups like Sunday Assembly) are equitably included, then the government is not providing direct subsidies or benefit to any specific religious or non-religious group or citizens. However, this again raises the issue of the IRS becoming arbiter and judge of what is a “true religion.”

Tax exemption and the church is highly controversial issue and if I am being honest, I’m not convinced that either side is outlandish – from either a secular or a religious point of view. In both cases there are pros and cons for the separation of church and state, for public benefit and for general equality. In fact, many churches have decided to not be classified as 501(c)(3)s, register with the IRS, and pay taxes like a general nonprofit would precisely because of the some of the reasons above, but mostly because they want to be able to perform any political activity they choose such as lobbying and campaign finance, without fear or government reprisal. While I have religious reasons to want to avoid that (if history has taught us anything, where the church enters the state, the state often is not far behind in coming into the church), I would ask the atheists if what they really want is a bunch of evangelicals who are angry about being forced to pay taxes now also able to official sponsor campaigns and lobby congress…

Although it is far from perfect, at the end of the day I find the benefit to simply weigh more heavily on keeping the tax exemptions in place to offer the best protection of the separation of powers and of the benefit to the community and her citizens.

Sources:

https://churchesandtaxes.procon.org/

https://www.nolo.com/legal-encyclopedia/are-churches-always-exempt.html

http://www.nydailynews.com/news/politics/churches-non-profits-play-politics-thanks-trump-article-1.3136449

https://www.reddit.com/r/PoliticalDiscussion/comments/3myrqd/why_is_planned_parenthood_who_receives_government/?st=jgo0lsgv&sh=b1065c31

https://www.irs.gov/newsroom/charities-churches-and-politics

https://www.bairdholm.com/publications-feed/entry/501-c-3-organizations-political-activity-and-lobbying.html

https://www.quora.com/Why-does-the-NRA-have-a-non-profit-tax-exempt-status

https://www.thebalancesmb.com/can-nonprofits-engage-in-political-activity-2501879

https://ffrf.org/outreach/item/12601-tax-exemption-of-churches

https://www.irs.gov/charities-non-profits/charitable-organizations/exemption-requirements-section-501c3-organizations

https://www.focusonthefamily.com/socialissues/religious-freedom/religious-freedom-after-the-obergefell-decision/why-are-churches-and-religious-organizations-tax-exempt

https://churchesandtaxes.procon.org/view.resource.php?resourceID=006554

https://www.forbes.com/sites/robertwood/2015/09/22/lets-tax-churches/#66fb0e6b322b

http://www.latimes.com/la-oew-lynn-stanley23-2008sep23-story.html

https://www.washingtonpost.com/news/in-theory/wp/2015/09/14/primer-tax-exemptions-for-religious-institutions/?noredirect=on&utm_term=.519b2c0ecb5f

https://www.thedailybeast.com/why-is-scientology-tax-exempt

No comments:

Post a Comment